![]()

2022 Realistic Verified Free CIMA F2 Exam Questions

F2 Real Exam Questions and Answers FREE

NEW QUESTION 92

WX acquired 60% of the equity shares of CD on 1 January 20X3. WX sold 5% of the equity shares it held for $60,000 on 31 December 20X5. At that date the net assets of CD were $120,000 and the fair value of the non-controlling interest in CD was measured at $21,000. No goodwill arose on the original acquisition of CD.

When preparing its consoldiated financial statements, WX will process which of the following adjustments to its group retained earnings?

- A. A debit of $54,000

- B. A credit of $39,000

- C. A credit of $54,000

- D. A debit of $39,000

Answer: C

NEW QUESTION 93

RST sells computer equipment and prepares its financial statements to 31 December.

On 30 September 20X5 RST sold computer software along with a two year maintenance package to a customer. The customer is given the right to return the goods within six months and claim a full refund if they are not satisfied with the computer software. The risk of return is considered to be insignificant for RST.

How should the revenue from this transaction and the right of return be recognised in the financial statements for the year ended 31 December 20X5?

- A. Recognise 12.5% of the revenue from both the sale of goods and the maintenance contract and do not create a provision for the anticipated level of returns.

- B. Recognise 100% of the revenue from both the sale of goods and the maintenance contract and create a provision for the anticipated level of returns.

- C. Recognise 100% of the revenue from the sale of goods,12.5% of the revenue from the maintenance contract and create a provision for the anticipated level of returns.

- D. Do not recognise any revenue from the sale of goods or the maintenance contract and do not create a provision for the anticipated level of returns.

Answer: C

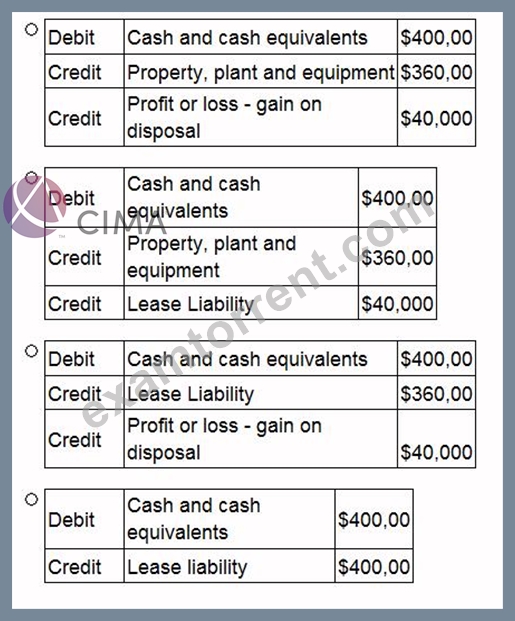

NEW QUESTION 94

ST has sold its main office property, which had a carrying value of $360,000, to AB, a property management entity.

The property was sold for $400,000 which is equal to its fair value and was immediately leased back under an operating lease agreement.

Which of the following journals will record this transaction?

- A. Option A

- B. Option B

- C. Option D

- D. Option C

Answer: A

NEW QUESTION 95

AB, a listed entity, prepared its financial statements to 31 December 20X7, in accordance with international accounting standards.

Which THREE of the following were disclosed as related parties of AB in its financial statements?

- A. AB's defined benefit pension plan.

- B. AB's main supplier, GH, who supplies more than 70% of AB's goods for manufacture.

- C. AB's bank that provides more than 60% of the entity's loan finance.

- D. The wife of the Managing Director of AB, to whom AB sold a motor vehicle in the year to 31 December 20X7.

- E. ST, an entity that was jointly established by AB and CD, and that is accounted for as a joint venture in AB's financial statements to 31 December 20X7.

Answer: A,D,E

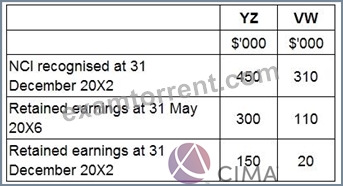

NEW QUESTION 96

AB acquired 90% of the equity of YZ on 31 December 20X2. On the same date YZ acquired 60% of the equity shares of VW for $750,000. AB has no other subsidiaries.

The following information regarding YZ and VW was available:

What amount will AB include in its consolidated statement of financial position in respect of non controlling interest at 31 May 20X6?

- A. $811,000

- B. $816,400

- C. $840,600

- D. $741,400

Answer: D

NEW QUESTION 97

AB acquired its subsidiary on 1 January 20X7 when the fair value of net assets was the same as book value with the exception of property, plant and equipment that had a fair value $500,000 higher than carrying value.

These assets were assessed to have a remaining useful life of 5 years from the date of acquisition.

What is the net consolidation adjustment to the property, plant and equipment balance at 31 December

20X9?

Give your answer to the nearest whole number (in '$000s).

$?

Answer:

Explanation:

200000, 200

NEW QUESTION 98

HJ is currently in dispute with an employee, who is claiming $400,000 in a legal case against them.

HJ's legal advisors have stated that it is probable that they will lose the case and will have to pay the amount claimed.

Also, HJ are claiming $250,000 from a supplier of defective goods and the legal advisors have stated that it is probable that HJ will be successful in this claim.

What is the correct accounting treatment for these two items in HJ's financial statements?

- A. Disclose the $400,000 potential outflow and disclose the $250,000 potential inflow.

- B. Provide for the $400,000 potential outflow and disclose the $250,000 potential inflow.

- C. Disclose the $400,000 potential outflow and recognise the $250,000 potential inflow.

- D. Provide for the $400,000 potential outflow and recognise the $250,000 potential inflow.

Answer: B

NEW QUESTION 99

XY owned 80% of the equity share capital of AB at 1 January 20X5. XY disposed of 20% of AB's equity share capital on 31 December 20X5 for $200,000. The non controlling interest was measured at

$140,000 immediately prior to the disposal.

What was the amount of the credit to retained earnings that XY will process in respect of this disposal when it prepares its consolidated financial statements at 31 December 20X5?

- A. $200,000

- B. $80,000

- C. $60,000

- D. $140,000

Answer: C

NEW QUESTION 100

A local council is one year into a two year project to renovate local parks. The project is on track to be completed within the set time-scale, however it has proved more costly than initially expected.

The project is on track to be completed within its two year period. Contracts for the labour and materials needed to renovate the parks were agreed at the start of the project and no changes have arisen. Despite the fact that the council has yet to fully settle these contracts, costs are set to be as budgeted.

Why would this example not be recognised as a provision?

- A. Neither the timing nor the amount of the provision is uncertain.

- B. The settlement of the contract is unlikely to result in an outflow from the council.

- C. The council has no potential future obligations arising from the project.

- D. The council doesn't have a present obligation from the project.

Answer: A

NEW QUESTION 101

Which of the following is NOT an example of an unconsolidated structured entity as defined in IFRS12 Disclosure of Interests in Other Entities?

- A. A securitisation vehicle

- B. An asset-backed financing scheme

- C. An investment fund

- D. A post-employment benefit plan

Answer: D

NEW QUESTION 102

Operating segments are separately reportable where they exceed 15% of revenue / profits / assets.

These must in total cover 80% of total revenue. Is this statement true or false?

- A. True

- B. False

Answer: B

NEW QUESTION 103

Company A are approached by a wealthy and internationally famous investor shortly before the launch date of their IPO. He tells them that the company do not need to incur all of the cost and risk of an IPO, as he will give them S55 million for 65% equity in the company.

Which of the following statements are also true of the offer? Select ALL that apply.

- A. The investor will probably want to manage the company

- B. This offer is from an angel investor

- C. The investor will want a long term commitment in the company

- D. The offer may ultimately require the majority stakeholder to sell his shares in the company

Answer: A,B,D

NEW QUESTION 104

XYZ had 600,000 ordinary shares in issue on 1 July 20X4. On 1 January 20X5, the entity made a 1 for 2 bonus issue. The profit attributable to ordinary shareholders for the year ended 30 June 20X5 was

$2,925,000.

What is the basic earnings per share for the year ended 30 June 20X5?

- A. $1.63

- B. $3.90

- C. $4.88

- D. $3.25

Answer: D

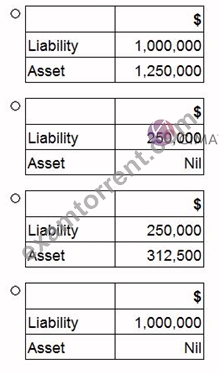

NEW QUESTION 105

The following information relates to DEF for the year ended 31 December 20X7:

* Property, plant and equipment has a carrying value of $3,500,000 and a tax written down value of

$2,500,000.

* There are unused tax losses to carry forward of $1,250,000. These tax losses have arisen due to poor trading conditions which are not expected to improve in the foreseeable future.

* The corporate income tax rate is 25%.

In accordance with IAS 12 Income Taxes, the financial statements of DEF for the year ended 31 December 20X7 would recognise deferred tax balances of:

- A. Option A

- B. Option B

- C. Option D

- D. Option C

Answer: A

NEW QUESTION 106

Which of the following would cause a deferred tax balance to be included in the statement of financial position for an entity?

- A. The acquisition of plant and equipment a year ago where the tax depreciation rate is different to the accounting depreciation rate.

- B. The acquisition of land for which there is no tax depreciation.

- C. Impairment of goodwill that arose on the acquisition of a subsidiary entity.

- D. Expenses in the statement of profit or loss which are not allowable for tax creating a permanent difference.

Answer: A

NEW QUESTION 107

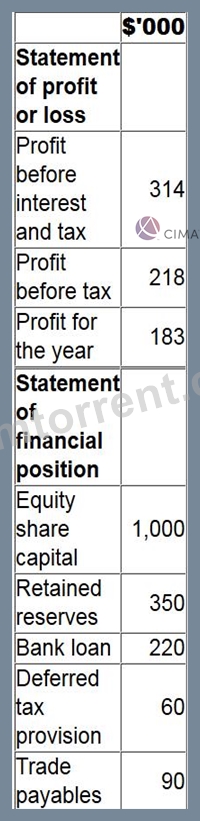

The following information is extracted from the financial statements of RS for the year ended 30 June 20X7:

RS has no other liability balances and has no associate investments.

Calculate return on capital employed for RS at 30 June 20X7.

Give your answer to the nearest whole %.

? %

Answer:

Explanation:

20

NEW QUESTION 108

LM has made the following share purchases during the year:

* Purchased 55% of the equity share capital of OP.

* Purchased 45% of the equity share capital of QR. LM have the power to appoint the majority of board members on the QR board.

* Purchased 30% of the equity share capital of ST. LM is represented by one director on the main board of ST which has five members in total. The other 70% of ST's equity share capital is owned by a single company, UV.

The Managing Director has told you that OP has performed well, but both QR and ST have not performed as expected. He is therefore pleased that OP will be included as a subsidiary and that QR and ST will only be included as investments in the group financial statements.

In accordance with the ethical principle of professional competence and due care how should the investments in OP, QR and ST be treated in the group financial statements?

- A. OP should be consolidated and QR and ST should be equity accounted.

- B. OP and QR should be consolidated and ST should be equity accounted.

- C. OP and QR should be equity accounted and ST should be valued at cost.

- D. OP should be consolidated, QR should be equity accounted and ST should be valued at cost.

Answer: B

NEW QUESTION 109

UV has raised $100,000 through the issue of two irredeemable financial instruments:

* 6% debentures with a current market value of $101.50 per $100 nominal value; and

* 8% preference shares with a current share price of $2.20 each.

The corporate income tax rate is 20%

What is the post tax cost of debt for each of these instruments?

Answer:

Explanation:

NEW QUESTION 110

......

Exam Dumps F2 Practice Free Latest CIMA Practice Tests: https://www.examtorrent.com/F2-valid-vce-dumps.html